Satire! 2,810 IC design companies only take 4% of the share, China's core calls for large-scale IDM

China Chip IDM

IC Insights, a world-renowned semiconductor analysis agency, disclosed information on the "Macklin Report 2022 Second Quarter Update" to be released in May, and used the rather eye-catching "Chinese companies only account for 4% of the global IC market share" as the title. , which caused widespread heated discussion in the industry for a while.

Source: IC Insights

In IC Insights' briefing titled "Chinese companies only account for 4% of the global IC market share", it is more about the rise of semiconductors in the United States and Asia, dominated by South Korea and Taiwan, China. There is only one sentence for mainland ICs: IDM The share is very low.

In the context of 592 new IC design companies in mainland China in 2021 (the current total number is 2,810), the figure of 4% is enough to alert the IC industry in mainland China. You must know that this figure is still 5% in 2020, and the sample data is already small. Next, the retreat of the mainland IC market is a year-on-year decline of 20%. In a sense, in this case, the more companies that appear, the more serious the involution of China's IC industry at the low end is. This is not a solution to the problem.

Although IC Insights only said one sentence about mainland IC in the briefing, it has already hit the door. Chinese chips need large-scale IDM, not only to compete with international manufacturers externally, but also to act as a catfish internally, forcing the mainland IC industry to upgrade.

Mainland IC can't expect "core" to catch fire

The beginning of the text may be a bit deep, so that the passionate mainland IC practitioners feel that cold water has been poured. In fact, in 2021, the first year of the "14th Five-Year Plan", if the mainland IC industry simply compares itself with itself, it will still open up a key situation at this special moment. According to the "Operation Situation of China's Integrated Circuit Industry in 2021" released by the China Semiconductor Industry Association, the sales of China's integrated circuit industry will reach 1,045.83 billion yuan in 2021, entering the trillion level for the first time, and the year-on-year growth rate of 18.2% is also higher than 17 in 2020. %.

However, it should be noted that the 1,045.83 billion yuan in 2021 not only includes 451.9 billion yuan in design industry sales, but also 317.63 billion yuan in manufacturing sales, and 276.3 billion yuan in packaging and testing industry sales. So, if we take the design industry out and get a better comparison to the IC Insights statistics, we get the following picture.

Data source: China Semiconductor Industry Association, Electronic Enthusiast Network Drawing

Obviously, in 2021, when we have more IC design companies, the year-on-year growth is not as good as the previous two years, and it has dropped to a level below 20%.

This is like a person who looks burly, but lacks strength and poor physique. We generally call it "puffy". There is no doubt that the IC design industry in mainland China is also "puffy". For "withered leaves" and "withered grass", they can't stand burning.

There is an old saying in China: one trades off and the other grows, and this is a very apt description of the total IC market share (the sum of IDM and fabless IC sales) in China and the US in 2021. IC Insights spent more of its presentation on the fact that the total US IC market reached 54%, a further increase of 4 percentage points compared to last year's 50%. The IC Insights chart below shows it well. Since 2005, the share of the United States in the total global IC market has been growing.

Source: IC Insights

Then, we can conclude that the rise of the mainland IC market (IDM and fabless IC) is a "small rise", while the rise of the US IC market is a "big rise". When the "rising" is merged together, because the original volume of the "small rising" is originally small, the "small rising" becomes the "no rising", and it also goes backwards.

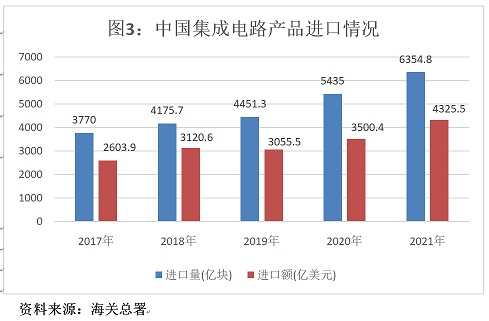

Recently, we have been talking about domestic substitution. When the mainland IC market has shrunk in the world, our substitution ratio has further shrunk, because we use the most chips in places. According to statistics from the General Administration of Customs, China will import 635.48 billion integrated circuits in 2021, a year-on-year increase of 16.9%; the import value will be 432.55 billion US dollars, a year-on-year increase of 23.6%.

Obviously, the idea of sparking a prairie fire goes against the capital-intensive, talent-intensive, and technology-intensive characteristics of integrated circuits. As Professor Wei Shaojun said, "Integrated circuits cannot make pigs in the wind." Among the 2,810 design companies in mainland China , 83.7% of the enterprises are small and micro enterprises with less than 100 employees, a total of 2351 enterprises. Of the 592 new IC design companies in 2021, 489 will have less than 100 employees. It seems to be a "prosperous scene" for the whole people to create cores, but most of them are aiming to get subsidies from various local governments, and then increase the involution of mainland IC companies in the low-end market, allowing them to cooperate with TI, ADI or Broadcom. It is obviously unrealistic to compete with international giants.

Chinese chip calls for large-scale IDM

More small and micro IC companies mean that more practitioners are only in the IC field. It is difficult for them to accumulate high-end experience by participating in large-scale projects. More experience is to repeat their work in specific functional areas. This is not helpful for the industry as a whole.

In this case, the mainland IC industry needs large-scale IDM manufacturers, and at this stage, Chinese chips need the IDM model to drive.

First of all, IDM manufacturers have the advantage of vertical integration, which can cover multiple industrial chain links such as design, manufacturing, packaging and testing, which means that IDM manufacturers can eat a field more thoroughly and realize industrial chain coordination, which is conducive to more Deeply and fully tap the technical potential of this field.

Secondly, the capability of IDM in the whole industry chain helps to promote technological innovation. We cannot deny that many small and micro IC companies in mainland China have technological innovation capabilities, but if they are not well connected, the foundry is likely to be Those who scoff at them will not take the initiative to cooperate with them.

Third, the IDM model has a stronger resource gathering ability, which is in line with the development characteristics of the integrated circuit industry, and the strong are always strong. Of course, IDM has also raised the entry barrier of the industry, but in fact we don't need so many small businesses, it is the local government who needs them.

In fact, Professor Wei Shaojun proposed very early that China needs IDM. His point of view at the time was that it was a must to go from OEM to self-owned brand, which has been verified in the fields of home appliances and clothing.

Continental IDM Status and Obstacles

According to relevant statistics, at present, global IDM manufacturers control almost 60% of the IC market share, which is still the mainstream. Mainland IC has been developing for so many years, and it is not completely ignoring the IDM model. There are also some manufacturers who know that this road is very difficult in the industrial environment of the mainland, but they still choose to carry the burden.

At present, dozens of companies in the mainland are following the IDM model, among which Wingtech Technology (subsidiary Nexperia), Tsinghua Unigroup and Silan Micro are the representatives. They have already issued scales, but there is still a gap between them and the international giants. In addition, China Resources Micro, Yangjie Technology, Suzhou Goodtech Electronics, Zhuzhou CRRC, BYD Microelectronics and other companies are also exploring the IDM model, showing a certain degree of vertical integration advantages in the field of power semiconductors and analog power devices.

However, many companies adopt the IDM model because of their products and their own needs, and have not yet formed scale and aggregation effects. In fact, there are many factors restricting the development of the IDM model of mainland ICs at present.

The first point is to talk about the scale. Of course, this is the weakness of the latecomers, and it can only be expanded a little bit.

The second point is the "flying pig idea", too many IC practitioners have the idea of "standing in the limelight, pigs can take off", so a few people, dozens or dozens of people pull the pole to engage in IC, the goal Most of them are subsidized, financed, and listed.

The third point is the concept of territory. At present, the IC industry has become a part of local governments to decorate their achievements, and set up their own support funds, and then grab and incubate enterprises. Let's look back at Professor Wei Shaojun's report at the time. In 2021, 21 cities in China will have IC companies with sales of over 100 million yuan. As shown in the figure below, practitioners are also deeply impressed. Most of the IC companies in these cities are independent. In other cities, there are many of their peers, and there are very few companies that can stand out like Huawei HiSilicon before. Therefore, many practitioners have publicly ridiculed, "Everyone is about the same level, who can look down on who?"

Data source: China Semiconductor Industry Association, Electronic Enthusiast Network Drawing

Originally, the overall scale was not large, and then each company wanted to dominate, and the local government also wanted to make political achievements. Then the final result must be that everyone dragged each other back, and the companies that really broke through the siege would have to peel off their skins in the internal friction. And waste a lot of money and energy in the process.

Obviously, the development of the mainland IC industry requires a higher level of authority to plan and lead, and then by concentrating resources to build IDM manufacturers in various fields, to build mainland IC's own brand. At this stage, although various companies say that their products are benchmarking against TI and Infineon, the result is that TI is still TI, and TI's products are still the mainstream.